The importance of cavern storage facilities will increase in the course of the energy transition. Caverns are artificially created cavities that are built in salt formations, for example in salt domes at great depths. Energy is stored in these cavities in liquid or gaseous form. These storage facilities are also to be used for hydrogen storage in the future. From the point of view of security of supply, these hydrogen storage facilities will have to store and withdraw energy for weeks and months at a time during periods of overproduction of electricity and during dark doldrums in the winter months. This makes the storage systems "enablers of the energy transition".

400 caverns needed by 2045

The analyses commissioned and published by the BMWK, summarised for example in the long-term scenarios and the green paper, show the necessary development of hydrogen storage facilities. In order to successfully transform the energy system in Germany, a storage capacity of at least 74 TWh of energy based on hydrogen must be built up and in operation by 2045. At the same time, oil and natural gas storage facilities will still need to be available in the energy system, albeit at a decreasing rate. It is assumed that, in addition to this estimate, additional hydrogen storage capacities will be required as a result of the expected power plant strategy.

Based on the average storage sizes of typical caverns with a capacity of around 0.2 TWhH2 thermal, around 400 caverns would have to be available on the market in 2045, taking into account the modelled storage capacities (see Fig. 1). Measured against the currently available storage capacities, new cavern fields are therefore also needed. Germany has by far the greatest potential for storing energy in underground storage facilities, which are also suitable for hydrogen, compared to all other European countries due to the outstandingly suitable natural salt rock formations and can expand this leading role in Europe.

The problem: However, due to the lack of prerequisites for investment decisions and the current legal approval periods, the development of underground storage facilities is not yet possible.

H2CAST Etzel" research project

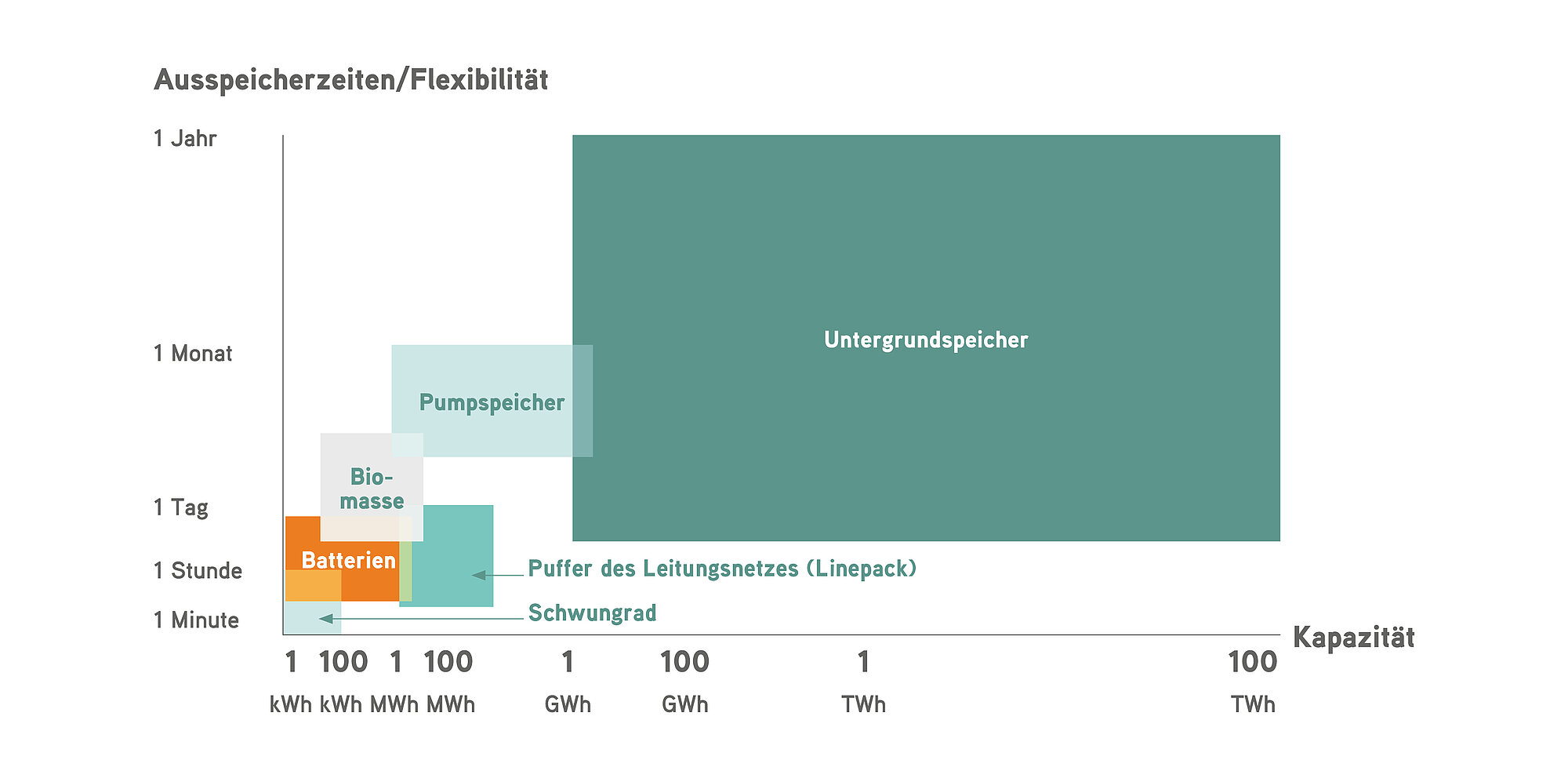

One solution could be to convert existing storage infrastructure. This is because cavern storage facilities are scalable and flexible (see Fig. 2), meaning that existing underground gas and oil storage facilities can also be repurposed for the use of hydrogen. Storag Etzel is currently investigating how this works in the "H2CAST Etzel" pilot and research project funded by the Federal Ministry for Economic Affairs and Energy and the state of Lower Saxony. Following extensive tests, the first caverns in Etzel have already been filled with small quantities of hydrogen (H2) and the project is making progress. The other announced project milestones are expected to be reached on schedule, with the first H2 cavern being transferred to licence-compliant operation by 2027. Further caverns could be available from 2028.

Long-term goal of making Etzel "H2-ready"

As the mine owner and system supplier for energy storage operators (SSO), Storag Etzel aims to make the Etzel cavern field "H2-ready". Due to the advantages of the location in combination with over 50 years of experience in developing large-volume caverns, the company has already created the legal basis for a hydrogen storage facility there over the last decade.

There are currently 51 natural gas storage caverns and 24 crude oil storage caverns in operation in Etzel. To this day, the caverns are an important part of the German and European energy supply. In addition to the operating caverns mentioned above, there are 24 potential caverns that have already been approved and can be completed within four to ten years in line with demand without any time risks. This corresponds to a storage capacity of six TWh without having to rededicate the storage facilities for natural gas that are already in operation.

Construction of necessary new H2 infrastructure

The need for a core network for the start of the hydrogen ramp-up is undisputed. In order to utilise the full potential of hydrogen as an energy carrier, mature considerations are required for safe transport through existing and new pipeline infrastructures. The primary framework conditions for core network planning make it clear that certain regions, particularly north-west Germany, are of strategic importance for a successful start to a new energy era.

Time is of the essence

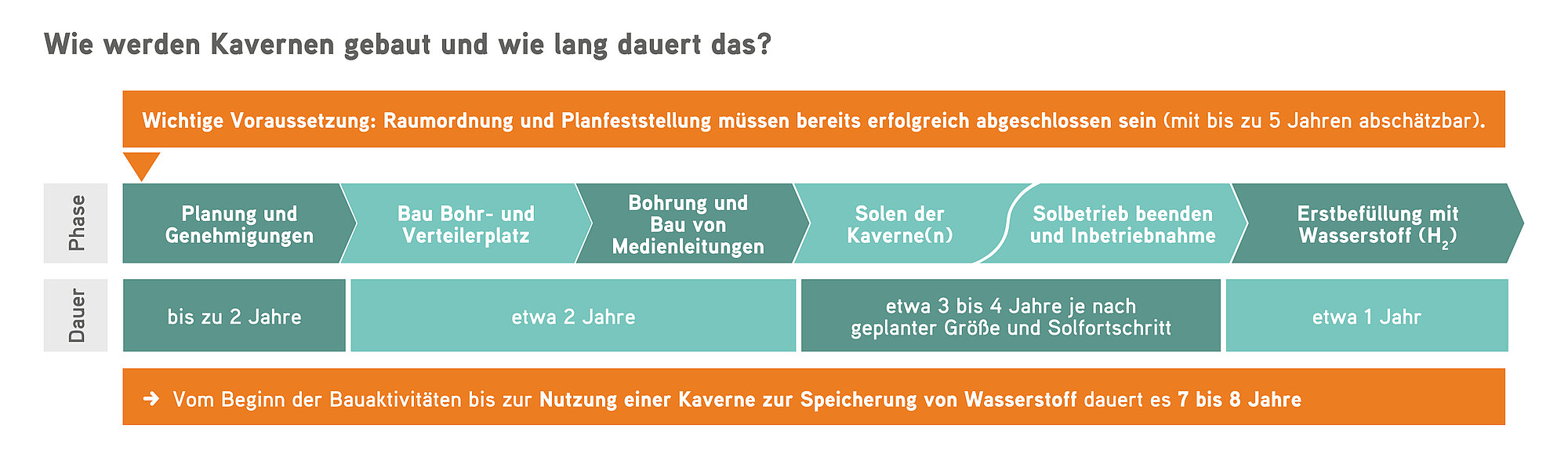

For hydrogen storage operations, the cavern storage facility must not only be connected to the pipeline infrastructure, but the energy storage operator (SSO) must also construct a suitable above-ground operating facility (including compressor and drying facilities). The planning, authorisation and construction of these operating facilities is expected to take six years. In addition to the complex planning and approval processes, this is also due to long delivery times for compressors and transformers, among other things, as well as mandatory tendering procedures. With an immediate start, i.e. an investment decision (FID) in 2024, the necessary above-ground operating facilities for feeding hydrogen in and out can be expected to be ready for operation from 2030. The following Fig. 3 shows the necessary authorisation and planning periods.

Fig. 3: Cavern field development / time estimate (Source: STORAG ETZEL)

The necessary H2 pipeline infrastructure must be constructed and in operation by this time at the latest, and the supply of hydrogen from imports and domestic production (e.g. electrolysis in the Wilhelmshaven area) must be ensured at the same time. This inevitably means that spatial planning concerns, changes and planning must begin today for the new construction of corresponding infrastructure projects. The authorities and public agencies involved must synchronise the approval processes with each other in order to be able to implement or construct the projects quickly.

Conclusion

The importance of cavern storage facilities and the construction of the necessary H2 infrastructure, which is crucial for the success of the energy transition in Germany, was outlined above. The following prerequisites must be created by federal policymakers:

- Authorisation procedures under mining law must be conducted in parallel or accelerated. In the case of the conversion of existing caverns or for cavern sites that have already been authorised and their above-ground facilities, complex and lengthy planning approval procedures with environmental impact assessments should be dispensed with.

- H2 storage will not have a business case for years to come, which means that in addition to hedging the investment risks (capex), it is also essential to subsidise the fixed operating costs (opex) for the energy storage operators (SSO).

- The contracts for differences (CfD) proposed by the German Storage Energy Initiative (INES), for example, offer the opportunity to realise the development and operation of hydrogen storage facilities by 2030 by commissioning companies to do so. The core idea of a contract for differences is that the difference between actual revenues and reference revenues, i.e. the shortfall in revenues, is compensated by the state, while excess revenues are repaid to the state. The reference revenues must inevitably include both capital costs (capex) and fixed operating costs such as rents to the cavern and mine owner (opex). Reference revenues could be determined by the regulator on the basis of a comprehensive project-specific cost review.

- The announced H2 storage strategy is still pending. Coordination is still required in 2024.

About STORAG ETZEL:

STORAG ETZEL GmbH is the largest independent provider of cavern storage facilities in Germany. At the Etzel site in East Frisia, the company has been building, maintaining and leasing underground storage capacity for gas and oil since 1971 and aims to make the site "H2-ready!" for the future as part of the H2CAST project.

Thanks to its unique geology, Etzel offers excellent conditions for the storage of liquid and gaseous energy sources. A massive salt dome at a depth of over 750 metres enables the safe storage of large quantities of gas, oil and hydrogen.

The Etzel site is also particularly suitable for the rapid expansion of underground storage facilities, as the large quantities of seawater required for brining caverns and the transport of brine can be carried out via existing transport pipelines to the North Sea and the necessary infrastructure is ready for use.

The tenants of the caverns are well-known energy trading companies and oil storage organisations from various European countries. The operator Storag Etzel has already successfully converted oil caverns to gas storage in its operating history.

About H2CAST Etzel

H2CAST Etzel (H2Cavern Storage Transition Etzel) focuses specifically on the adaptation and repurposing of existing gas caverns and relevant above-ground facilities as part of the transition process to an H2 economy in Germany and Europe. The industrial scalability of the underground storage facilities and above-ground facilities at the Etzel cavern site is a particular speciality here.

The Etzel pipeline and grid hub in particular offers a wide range of cooperation and funding opportunities for the development of an H2 economy in the Friesland/East Friesland/Wilhelmshaven region in north-west Germany.

The integration of power generation from offshore wind energy, Etzel's cross-border pipeline connection to the Netherlands and the possible import of H2 by ship via an H2 terminal at the deep-water harbour in nearby Wilhelmshaven also offer opportunities for expansion.